In recent years and months, the volume of sustainable investment has grown continuously. Globally, sustainable bond issuance, including green, social, sustainability, and sustainability-linked bonds, could collectively exceed $1 trillion in 2021, a near 5 times increase over 2018 levels, according to S&P Global Ratings[1].

At the same time, the climate crisis, the loss of biodiversity and social inequality, three of the most critical problems worldwide, are also increasing. Consumers, workers, and society in general demand concrete answers to these and other problems.

Concomitantly, the increase and mismanagement of waste is becoming increasingly important. For an investor – even those who have not yet understood the importance of sustainability or ESG – waste is inefficiency. The foremost Michael Porter, a Harvard professor and the guru behind the concept of “competitive advantage”, had already explained it in 1995: “Pollution is often a form of economic waste”. When waste, harmful substances or forms of energy are discharged into the environment as pollution, it is a sign that resources have been used incompletely, inefficiently, or ineffectively. In addition, companies must perform additional activities that add costs, but do not create value for customers: for example, handling, storage and disposal of byproducts.”[2] For society in general and especially the environment, waste represents something even worse, such as the loss of biodiversity and, albeit indirectly, climate change.

In this context, measuring waste, with metrics accepted and understood globally by investors and other interested parties, is becoming a mandatory requirement for various sectors and far beyond legal obligations. But what are the most important metrics? How to optimize measurement and production systems to effectively generate less waste or inefficiency?

Answering the second question in this article would be impossible, since the answer depends on a complex diagnostic work of each activity, its environmental aspects, and impacts. But it is possible to at least try to answer the first question.

Obviously, there is no global regulation on waste or waste metrics. The only exception would be the International Convention for the Prevention of Pollution from Ships, the MARPOL Convention, adopted in 1973[3], but valid only for a niche in the economy.

In this context, voluntary reporting standards emerge, highlighting the GRI (Global Reporting Initiative) standards and the SASB (Sustainability Accounting Standards Board) standards.

The GRI standards are transversal, valid for any sector and consider investors and other interested parties. SASB‘s standards are sectorial, although quite ambitious, covering 77 sectors, and are basically focused on the demands of investors.

The GRI standards are designed for organizations to present information about their impacts on the economy, the environment and society. They are structured as a set of universal interrelated standards (GRI 101, 102 and 103) and thematic standards: GRI 200 series, with specific requirements for economic issues, 300 series, covering environmental issues and 400 series for social issues. They have been developed primarily to be used together to help organizations produce sustainability reports that are based on the Principles for Reporting and focus on so-called material or more important topics[4]. Each standard contains requirements – detailed in this article – as well as recommendations and guidelines.

GRI 306 (2020) standard: Waste

In 2020, GRI published a new edition of the GRI 306 standard, dedicated exclusively to waste, replacing the 2016 version, which also dealt with effluents.

The GRI 306 standard recognizes that “Waste can be generated in the organization’s own activities, for example, during the production of its products and delivery of services. It can also be generated by entities upstream and downstream in the organization’s value chain, for example, when suppliers process materials that are later used or procured by the organization, or when consumers use the services or discard the products that the organization sells to them. Waste can have significant negative impacts on the environment and human health when inadequately managed. These impacts often extend beyond locations where waste is generated and discarded. The resources and materials contained in waste that is incinerated or landfilled are lost to future use, which accelerates their depletion.”[5]

The standard includes content on the management approach and thematic content. These are listed in the standard as follows and with the following requirements or metrics:

Management Approach disclosures

- Disclosure 306-1 Waste generation and significant waste-related impacts

The reporting organization shall report the following information: a. For the organization’s significant actual and potential waste-related impacts, a description of: i. the inputs, activities, and outputs that lead or could lead to these impacts; ii. whether these impacts relate to waste generated in the organization’s own activities or to waste generated upstream or downstream in its value chain.

- Disclosure 306-2 Management of significant waste-related impacts

- Actions, including circularity measures, taken to prevent waste generation in the organization’s own activities and upstream and downstream in its value chain, and to manage significant impacts from waste generated. b. If the waste generated by the organization in its own activities is managed by a third party, a description of the processes used to determine whether the third party manages the waste in line with contractual or legislative obligations. c. The processes used to collect and monitor waste-related data.

Topic-specific disclosures

- Disclosure 306-3 Waste generated

- Total weight of waste generated in metric tons, and a breakdown of this total by composition of the waste. b. Contextual information necessary to understand the data and how the data has been compiled.

- Disclosure 306-4 Waste diverted from disposal

- Total weight of waste diverted from disposal in metric tons, and a breakdown of this total by composition of the waste. b. Total weight of hazardous waste diverted from disposal in metric tons, and a breakdown of this total by the following recovery operations: i. Preparation for reuse; ii. Recycling; iii. Other recovery operations. c. Total weight of non-hazardous waste diverted from disposal in metric tons, and a breakdown of this total by the following recovery operations: i. Preparation for reuse; ii. Recycling; iii. Other recovery operations. d. For each recovery operation listed in Disclosures 306-4-b and 306-4-c, a breakdown of the total weight in metric tons of hazardous waste and of non-hazardous waste diverted from disposal: i. onsite; ii. offsite. e. Contextual information necessary to understand the data and how the data has been compiled.

- Disclosure 306-5 Waste directed to disposal [6]

- Total weight of waste directed to disposal in metric tons, and a breakdown of this total by composition of the waste. b. Total weight of hazardous waste directed to disposal in metric tons, and a breakdown of this total by the following disposal operations: i. Incineration (with energy recovery); ii. Incineration (without energy recovery); iii. Landfilling; iv. Other disposal operations. c. Total weight of non-hazardous waste directed to disposal in metric tons, and a breakdown of this total by the following disposal operations: i. Incineration (with energy recovery); ii. Incineration (without energy recovery); iii. Landfilling; iv. Other disposal operations. d. For each disposal operation listed in Disclosures 306-5-b and 306-5-c, a breakdown of the total weight in metric tons of hazardous waste and of non-hazardous waste directed to disposal: i. onsite; ii. offsite. e. Contextual information necessary to understand the data and how the data has been compiled.

SASB standards and waste

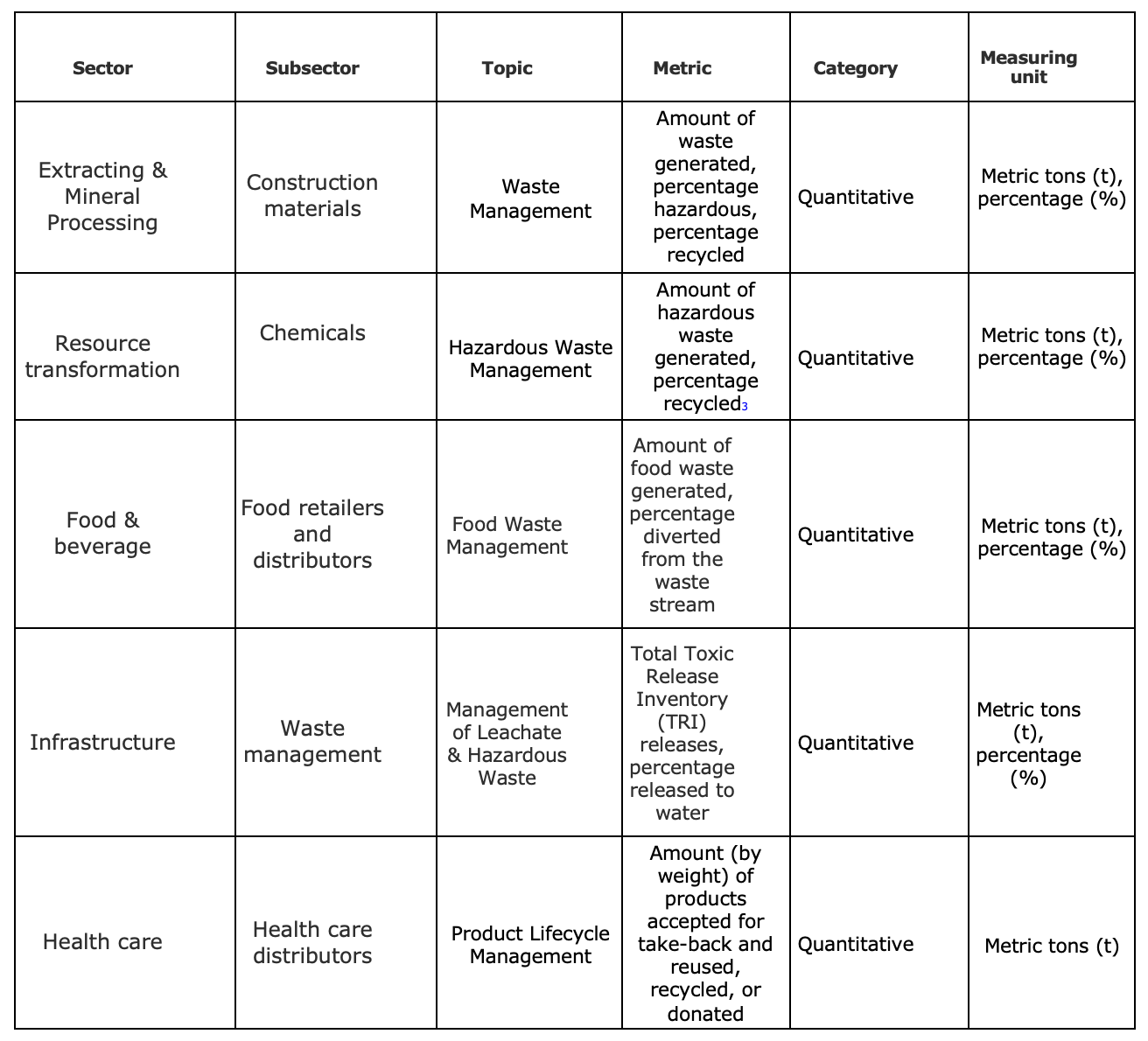

The topic “management of waste and hazardous materials” appears prominently in several SASB sectoral standards:

- Sectors: Extracting & Mineral Processing, and Resource Transformation, in which “the issue is likely to be material for more than 50% of industries in sector”

- Sectors: Food & Beverage; Health Care; Infrastructure; Renewable Resources and Alternative Energies; Technology & Communications, and Transportation, in which “the issue is likely to be material for fewer than 50% of industries in sector“[7]

Examples of metrics:

On the other hand, it is interesting to note that waste does not appear as material issues in sectoral standards such as those of the entire Consumer Goods sector, but also, and more intuitively, in the standards of the Financial and Services sectors. It is also striking that waste does not appear in the regulations of subsectors such as Oil and Gas – Services or Agricultural Products. These absences can be explained by the focus on investors of the SASB standards and mainly by the focus on environmental, social and other really more critical issues. SASB standards have an average of 6 material topics per industry standard.

Conclusion

Measuring sustainability, especially environmental issues like waste, is becoming increasingly important and easier, due to a growing consensus and convergence worldwide. As highlighted in this article, the GRI and SASB standards provide quite specific qualitative and quantitative metrics on waste, hazardous materials, and circularity. ESG metrics are the main “vaccine” against greenwashing. Without metrics, there is no ESG.

Article by our founder Marcio Viegas, published in the magazine Futurenviro on October 1 , 2021.

[1] https://www.spglobal.com/ratings/en/research/articles/210823-the-fear-of-greenwashing-may-be-greater-than-the-reality-across-the-global-financial-markets-12074863

[2] Porter, M & van der Linde, C. Green and Competitive: Ending the Stalemate. Harvard Business Review. September–October 1995. https://hbr.org/1995/09/green-and-competitive-ending-the-stalemate

[3] https://www.imo.org/es/About/Conventions/Pages/International-Convention-for-the-Prevention-of-Pollution-from-Ships-(MARPOL).aspx

[4] https://www.globalreporting.org/standards/media/1036/gri-101-foundation-2016.pdf

[5] https://www.globalreporting.org/media/ikhf0ggk/gri-306-waste-2020.pdf

[6] id

[7] SASB. SASB Materiality Map. https://materiality.sasb.org/